A budget forecast in operations planning can look calm on a spreadsheet while pressure builds underneath it. The plan may show labor, inventory, shipping, capacity, maintenance, software costs, and supplier spend in neat rows. Real operations are less tidy. Demand shifts, lead times stretch, overtime appears, equipment needs attention, and small cost assumptions begin to lean on each other like loose shelves in a stockroom.

That is why budget forecasting mistakes in operations planning are rarely just “finance mistakes.” They affect staffing, service levels, delivery promises, production schedules, cash timing, vendor decisions, and the daily choices managers make when resources are tight.

Safe Reading Note: This article is for general operational planning education. It is not financial, legal, accounting, or investment advice. Each business should review its own numbers, contracts, controls, and planning needs with qualified professionals when needed.

Why Budget Forecasting Is Risky in Operations Planning

Operations planning connects money to action. A forecast is not only a future number; it often becomes the basis for hiring, purchasing, production slots, warehouse space, supplier commitments, system upgrades, and customer promises.

The risk appears when the forecast is treated as if it were more certain than it really is. A team may plan around a single demand number, a single labor rate, a single supplier lead time, or a single “normal month.” That can work when conditions stay stable. It can fail quietly when one assumption moves.

In smaller projects, the damage may be limited to missed deadlines, awkward vendor calls, or a few weeks of overtime. In larger systems, the same mistake can create excess inventory, service delays, burned-out teams, cash strain, or a budget that loses credibility before the planning period is halfway over.

Common Wrong Assumptions Behind Weak Forecasts

Many budget problems start before the first formula is written. They begin with assumptions that feel reasonable because everyone has heard them before.

- “Last year is a safe baseline.” It may be, but only if demand mix, pricing, staffing, supplier terms, and operating constraints are still similar.

- “Average cost is good enough.” Averages can hide peak-season overtime, expedited freight, low-volume product costs, or uneven maintenance needs.

- “Finance can build the forecast alone.” Finance may own the model, but operations often knows the friction: capacity limits, downtime, scrap, returns, backlog, and shift coverage.

- “A forecast becomes useful once it is approved.” Approval does not make a forecast usable. Monitoring, variance review, and update rules matter just as much.

- “If sales grows, the operation can scale with it.” Sometimes it can. Sometimes the bottleneck is people, space, equipment, supplier capacity, or working capital.

Planning Reality: A budget forecast should not behave like a locked door. It works better as a controlled planning map: clear enough to guide decisions, flexible enough to update when the ground changes.

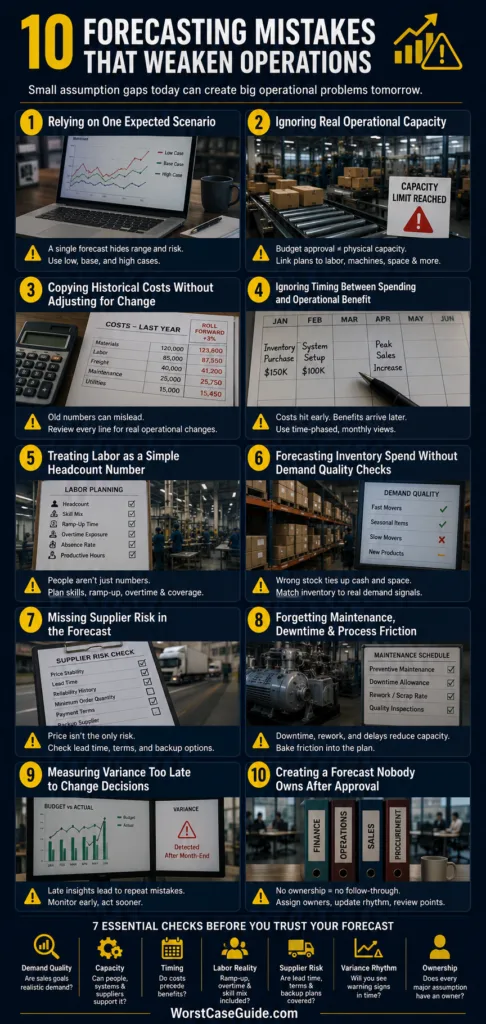

10 Budget Forecasting Mistakes in Operations Planning

Mistake 1: Building the Forecast Around One Expected Scenario

A single forecast number can feel clean. It is easy to explain. It is also fragile. Operations planning usually needs more than one possible path because demand, supplier timing, labor availability, and customer behavior rarely move in perfect lines.

Why It Happens

Teams may be under time pressure. Leaders may ask for “the number.” Planning tools may be designed around one approved budget rather than multiple operating scenarios. The result is a forecast that looks precise but does not show the range of possible outcomes.

Early Warning Signs

- The plan has no low, base, and high case.

- There is no clear view of what happens if demand drops or rises faster than expected.

- Inventory, staffing, and supplier commitments are based on one demand curve.

- Managers discuss variance only after the month closes.

Worst-Case Result

The operation may be overbuilt for demand that never arrives, or underprepared for demand that does. In a low-demand case, this can leave the business with excess stock, unused labor hours, and fixed costs that are hard to unwind. In a high-demand case, customers may face delays while teams pay more for overtime, rush shipping, and emergency procurement.

Safer Approach

A more stable forecast uses scenario planning. The team can define a realistic base case, a slower case, and a pressure case. Each scenario should connect to operational choices: hiring triggers, stock buffers, supplier commitments, shift changes, maintenance timing, and cash needs.

Mistake 2: Separating the Budget From Real Operational Capacity

A forecast may show that the business can afford production, fulfillment, or service delivery. That does not mean the operation can physically perform it. Budget approval and operational capacity are not the same thing.

Why It Happens

Budget models often focus on cost categories: payroll, materials, freight, software, rent, and outside services. Operations planning also needs constraints: machine hours, warehouse space, pick rates, training time, supplier capacity, inspection time, and maintenance windows.

Early Warning Signs

- The budget grows revenue or output without checking labor hours or equipment limits.

- Capacity planning is handled in a separate file from the budget forecast.

- Supervisors say the plan “works on paper” but not on the floor.

- Backlog, downtime, rework, and queue time are not included in planning conversations.

Worst-Case Result

The business may accept demand it cannot serve well. That can lead to missed delivery windows, quality shortcuts, higher returns, staff fatigue, and customer trust issues. The budget may still appear controlled for a while, but operations becomes the place where hidden cost collects.

Safer Approach

The forecast should be tied to capacity assumptions. If output rises by 20%, the plan should show what must also rise: trained labor, supplier availability, storage space, quality checks, support capacity, and management attention. If one constraint cannot move, the forecast should reflect that limit.

Mistake 3: Using Historical Costs Without Adjusting for Operational Changes

Last year’s numbers can be useful. They can also mislead. A budget forecast that copies historical costs without asking what changed may carry old reality into a new operating period.

Why It Happens

Historical data feels safe because it is real. Teams may roll forward prior-year numbers and add a small percentage. This can miss changes in product mix, supplier terms, wage rates, service expectations, equipment age, return rates, or delivery geography.

Early Warning Signs

- The forecast uses “last year plus percentage” across many expense lines.

- New products, new routes, new customers, or new systems are not modeled separately.

- Cost per order, cost per unit, or cost per service case is assumed to stay flat.

- Older equipment is budgeted as if maintenance needs will remain stable.

Worst-Case Result

The plan may understate the real cost of serving the business. A new customer segment may require more support. A different product mix may need more handling time. A broader delivery area may raise freight costs. The forecast then becomes a rearview mirror, not a planning tool.

Safer Approach

Historical numbers can remain the starting point, but each major line should be checked against operational change. A simple review question helps: What is different about how the work will be done this period? The answer often points to the cost lines that need fresh assumptions.

Mistake 4: Ignoring Timing Differences Between Spending and Operational Benefit

Some costs arrive before the benefit appears. Hiring, training, inventory purchases, system setup, maintenance, and supplier deposits may all require spending ahead of output. A budget that misses timing can look profitable while cash or capacity becomes tight.

Why It Happens

Annual forecasts often smooth costs across months. Operations does not always behave that way. A warehouse may need stock before peak season. A team may need training before volume arrives. A system may require setup months before it improves workflow.

Early Warning Signs

- The forecast is annual, but purchasing and hiring decisions are monthly or weekly.

- Large setup costs are spread evenly without checking cash timing.

- Inventory purchases are planned close to the same month as expected sales.

- Training time is budgeted as if new hires are productive immediately.

Worst-Case Result

The operation may run short of cash, people, or materials at the exact moment it needs flexibility. A team may then delay purchases, cut preparation time, or rely on expensive last-minute options. Small timing gaps can become large operational stress.

Safer Approach

The budget forecast should include time-phased planning. Monthly or weekly views can show when money leaves, when capacity becomes available, and when benefits are expected. For seasonal businesses, this matters even more.

Mistake 5: Treating Labor as a Simple Headcount Number

Labor forecasting is not only about how many people are on the payroll. Skill mix, shift coverage, learning curves, overtime limits, absence rates, supervision, and handoff quality all affect operational cost.

Why It Happens

Headcount is easy to budget. Real work is messier. Two employees with different training levels may not create the same capacity. A new hire may need weeks before reaching normal productivity. A small gap in one specialist role can slow an entire workflow.

Early Warning Signs

- The forecast uses average salary but not productivity ramp-up.

- Overtime is treated as a rare exception even though it appears every month.

- Training, onboarding, absence coverage, and supervisor time are missing.

- One experienced person is quietly carrying a process that the plan assumes is shared.

Worst-Case Result

The business may approve a labor budget that cannot support the work. Teams can become dependent on overtime, informal shortcuts, or one overloaded employee. Service quality may drift before leadership sees the full cost.

Safer Approach

A safer labor forecast separates headcount, skill coverage, productive hours, ramp-up time, and overtime exposure. In smaller teams, even one vacancy can change the plan. In larger operations, small errors in productivity assumptions can create large monthly variances.

Mistake 6: Forecasting Inventory Spend Without Demand Quality Checks

Inventory decisions often turn forecast errors into physical problems. Too little stock can delay orders. Too much stock can tie up cash, take space, age poorly, or hide weak demand signals.

Why It Happens

Teams may use sales targets as demand forecasts. They may also group products together and miss the difference between fast-moving items, slow-moving items, seasonal demand, and one-off customer orders.

Early Warning Signs

- Inventory budgets are based mainly on revenue goals.

- Slow-moving stock is not reviewed before new purchases are approved.

- Forecast accuracy is measured only in total, not by product group or location.

- Procurement decisions are made before demand assumptions are challenged.

Worst-Case Result

The operation may spend heavily on the wrong stock while running short of the items customers actually need. This creates a strange double problem: cash is tied up, yet service still suffers.

Safer Approach

Inventory forecasting should connect budget, demand planning, lead time, storage limits, and service targets. Product segmentation helps. Fast-moving items, seasonal items, long-lead items, and uncertain items should not all be planned with the same rule.

Mistake 7: Missing Supplier Risk in the Budget Forecast

A supplier price may be written into the budget, but the real operational risk may sit in minimum order quantities, lead time, delivery reliability, contract terms, quality issues, or backup supplier costs.

Why It Happens

Forecasts often capture the expected unit price and ignore the conditions around it. A lower quoted cost may depend on larger order volumes, longer commitments, fewer delivery windows, or less flexibility.

Early Warning Signs

- The budget assumes stable supplier pricing without checking contract terms.

- No separate allowance exists for expedited freight or alternate sourcing.

- Lead-time changes are discussed informally but not reflected in the forecast.

- Procurement has concerns that are not visible in the planning model.

Worst-Case Result

A supplier issue can force the business into higher-cost buying at short notice. Production may slow, service teams may wait for parts, or customer delivery dates may slip. The budget variance then appears as a cost problem, even though the first weakness was supplier planning.

Safer Approach

Supplier assumptions should include price, lead time, reliability, minimum order rules, payment terms, and backup options. Where one supplier is essential, the forecast should show what a delay or price change would do to operations.

Mistake 8: Forgetting Maintenance, Downtime, and Process Friction

Operations plans often budget for normal activity. They may forget the quiet drag of maintenance, downtime, rework, handoffs, approvals, inspections, system outages, and process delays.

Why It Happens

These costs are easy to treat as background noise. They may be spread across departments, hidden inside labor time, or described as “just how the process works.” A forecast that ignores them can overstate available capacity.

Early Warning Signs

- Equipment is budgeted as if it will run at full planned capacity.

- Rework, scrap, returns, and corrections are not tracked clearly.

- System downtime is discussed only after it disrupts work.

- Maintenance is delayed to protect short-term budget numbers.

Worst-Case Result

The business may save money in the budget and lose it in operations. Deferred maintenance can lead to longer downtime. Poor process visibility can turn small defects into repeated corrections. The forecast then becomes too clean for the real workflow.

Safer Approach

The planning model should include normal downtime, preventive maintenance, quality checks, rework rates, and process delays where they affect output. This does not need to be dramatic. It needs to be honest.

Mistake 9: Measuring Variance Too Late to Change Decisions

Variance review is useful only if it can influence the next decision. If budget differences are discovered after orders are placed, shifts are scheduled, stock is purchased, or contracts are signed, the forecast becomes a history report.

Why It Happens

Many teams review budget performance monthly or quarterly. That may be enough for some overhead costs. It may be too slow for operations where spending decisions happen daily.

Early Warning Signs

- Managers learn about budget problems after the month closes.

- Operational metrics and budget reports are reviewed in separate meetings.

- There is no trigger for revising the forecast when demand changes.

- Variance explanations repeat each month without changing planning rules.

Worst-Case Result

The same error repeats until it becomes expensive. Teams may overspend on avoidable overtime, buy stock too early, underprepare for demand, or miss a supplier issue that was visible in operational data before it hit the financial report.

Safer Approach

Variance monitoring should connect finance and operations. Useful triggers may include forecast accuracy changes, backlog growth, overtime thresholds, supplier delays, inventory aging, and service-level dips. The goal is not to chase every small number. It is to catch patterns early enough to respond.

Mistake 10: Creating a Forecast Nobody Owns After Approval

A budget forecast can lose value when everyone helps approve it but no one owns the follow-through. The document exists, yet decisions move around it.

Why It Happens

Budget ownership is sometimes vague. Finance may manage the model. Operations may manage the work. Department leaders may control spending. If the handoff is unclear, the forecast becomes a shared file with no shared discipline.

Early Warning Signs

- No one is assigned to update operational assumptions.

- Budget owners and process owners are not the same people.

- Forecast changes happen in side conversations rather than a visible process.

- Teams debate whose number is “right” instead of deciding what changed.

Worst-Case Result

The budget may stop guiding decisions. Teams may create unofficial spreadsheets, use different versions of demand, or approve spending based on outdated assumptions. Trust drops. Once that happens, even a good forecast can be ignored.

Safer Approach

Forecast ownership should be clear after approval. Each major assumption needs an owner, an update rhythm, and a review point. Operations, finance, procurement, sales, and service leaders may all hold part of the picture. The value comes from keeping those parts connected.

Risk Comparison Table for Budget Forecasting Mistakes

| Mistake Area | Where the Risk Appears | Early Signal | Safer Planning Check |

|---|---|---|---|

| Single Scenario | Demand, staffing, inventory, cash | No low or high case exists | Use scenario-based planning triggers |

| Capacity Gap | Production, fulfillment, service delivery | Output grows faster than available capacity | Link budget lines to operational constraints |

| Historical Cost Copying | Materials, labor, freight, maintenance | Costs are rolled forward without change review | Test each line against operational changes |

| Poor Timing View | Cash, hiring, training, inventory | Annual budget hides monthly pressure | Build a time-phased forecast |

| Weak Ownership | Forecast updates, accountability, decisions | No one owns assumptions after approval | Assign owners and review points |

General Risk Patterns That Repeat Across Weak Forecasts

Budget forecasting mistakes often look different by department, but the pattern underneath is similar. The forecast becomes weak when it loses contact with how work actually happens.

The Forecast Is Too Smooth

Operations has spikes. Peak weeks, supplier delays, onboarding periods, batch work, returns, maintenance windows, and customer surges can all make spending uneven. A smooth forecast may hide the real pressure points.

The Forecast Uses Finance Language but Not Operations Language

Finance may speak in cost centers and expense lines. Operations may speak in units, shifts, pallets, tickets, routes, service calls, cycle time, scrap, downtime, and backlog. Both languages matter. When one is missing, the forecast can become hard to use.

The Forecast Rewards Approval More Than Learning

Some teams treat a forecast as a document to defend. That can make people slow to admit when assumptions changed. A healthier approach treats forecast changes as useful signals, not personal failure.

The Forecast Hides Trade-Offs

Lower inventory may protect cash but increase stockout risk. Lower labor spend may protect the budget but raise overtime later. Cheaper suppliers may reduce unit cost but add lead-time risk. Operations planning is full of trade-offs, and the forecast should make them visible.

A Useful Planning Test: If the forecast changed by 10% tomorrow, would the team know which decisions should change with it? If not, the forecast may be acting more like a static report than an operating plan.

How Different Situations Change the Risk

If You Are Planning a Smaller Operation

In a smaller operation, the biggest risk is often dependency. One supplier, one experienced employee, one warehouse process, or one large customer can shape the whole budget. The forecast may need fewer lines, but each assumption carries more weight.

If You Are Planning a Larger System

In larger systems, the danger is usually distance. Finance may be far from the floor. Procurement may see supplier risk before operations does. Sales may change demand expectations before staffing plans update. The forecast needs clear coordination, or slow communication becomes a hidden cost.

If Demand Is Seasonal

Seasonal demand makes timing more important than annual totals. A forecast can be accurate for the year and still fail during the peak month. Inventory, temporary labor, training, delivery capacity, and customer support should be planned around the season, not just the annual budget.

If the Business Is Changing Fast

When products, customers, suppliers, systems, or locations are changing, old averages become less reliable. The forecast should show what is known, what is assumed, and what needs review. That small bit of honesty can prevent a lot of cleanup later.

Practical Checks Before Trusting an Operations Budget Forecast

A forecast does not need to be perfect to be useful. It needs to show where the business is making assumptions and where those assumptions could bend.

- Check demand quality: Are sales goals separated from realistic demand signals?

- Check capacity: Can people, suppliers, systems, space, and equipment support the planned volume?

- Check timing: Do costs appear before the benefit, and is that visible month by month?

- Check labor reality: Are ramp-up time, overtime, absence, and skill mix included?

- Check supplier exposure: Are lead time, minimum orders, backup options, and payment terms reflected?

- Check variance rhythm: Will the team see warning signals soon enough to change decisions?

- Check ownership: Does each major assumption have a named owner?

FAQ

What Is a Budget Forecast in Operations Planning?

A budget forecast in operations planning estimates future spending and resource needs for work such as staffing, production, inventory, logistics, maintenance, systems, and supplier activity. It helps teams plan how money, capacity, and timing may connect to daily operations.

Why Do Budget Forecasts Fail in Operations?

Budget forecasts often fail when they rely on fixed assumptions, old cost patterns, weak demand signals, or finance-only inputs. Many failures come from missing operational limits such as labor capacity, supplier lead time, equipment downtime, space, or process bottlenecks.

How Often Should an Operations Budget Forecast Be Updated?

The update rhythm depends on the business. Stable operations may review monthly. Fast-moving or seasonal operations may need weekly checks on demand, inventory, labor, supplier delays, backlog, and overtime. The forecast should be reviewed often enough to influence real decisions.

What Is the Difference Between a Budget and a Forecast?

A budget is often an approved plan for a period. A forecast is usually a refreshed estimate based on newer information. In operations planning, the budget may set the target, while the forecast helps teams adjust to what is actually happening.

What Metrics Help Detect Budget Forecasting Problems Early?

Useful warning metrics may include forecast accuracy, overtime hours, backlog, service levels, inventory aging, stockouts, supplier delays, downtime, rework, scrap, rush shipping, and monthly variance by cost driver. The right mix depends on the operation.

Should Operations and Finance Build the Forecast Together?

Usually, yes. Finance can bring budget discipline, reporting structure, and cost visibility. Operations can bring real workflow knowledge, capacity limits, supplier issues, labor constraints, and timing risks. A forecast is stronger when both views are connected.